If you have been up and about the lending community, credit score should have crossed your path. Based on research, it has been found that although people heard about credit score and how it affects the fate of one’s loan application, they hardly understand what a fair credit score is all about. That’s probably because there are myths surrounding it and that people do not really pour in time to learn more about it. Here are top 10 myths and the realities behind them so you will understand not just what a credit score is but also how you can achieve a fair rating that will do wonders in your loan applications.

10. Myth: Working with a debt settlement company can do wonders.

Fact: Working with a debt settlement company can further worsen your credit score.

What you should do, instead of entrusting your debt payment funds to a company that is only directed to earn through you, is to seek a non-profit credit counselor’s help. A credit counselor could negotiate in your behalf. This way, you will be doing settlement by yourself. You will not need to pay fees to a debt settlement company and even suffer the consequence of harassing phone calls from your creditors and a significantly lower credit rating. If you want a good credit score, you should be well-guided by reputable credit counselors and not by some company that could only make your problem worse.

9. Myth: When you get married, your spouse’s credit rating will be combined with yours.

Fact: A credit report is individual.

You cannot combine your credit information with another. Although it is possible that one item can be reflected on both your and your spouse’s credit report, you cannot marry one with a good rating and expect your score to go up. The kind of information shared between spouses is usually regarding joint accounts or credit accounts that you hold with your better half.

8. Myth: Your age and your income affect your score.

Fact: When credit bureaus evaluate scores, they do not take into account factors such as age, sex, length of employment, and amount of compensation.

Your credit score is used to gauge your creditworthiness. They are merely provided to ensure lenders that they can retrieve their credits back right on time. That’s why the things that matter in measuring one’s score are one’s track record in paying debts on time.

7. Myth: Negative information can be erased from your credit history to boost your score.

Fact: No accurate information can be legally removed from your credit history.

Only time can remove the blemishes in your files. So the key to ensuring a better credit score in the future is to start now in putting everything in order. In time, all those bad ratings will disappear. You do not need a company to create a new credit identity for you, minus all the accurate negative information because that is not possible.

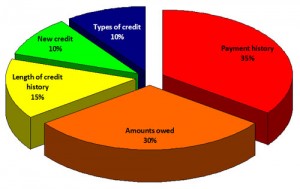

6. Myth: Paying off old debts and closing them will boost your score.

Fact: Closing old accounts could reduce your credit history, which forms 15% of your score.

If you close an old credit account, you could hurt it than help it. Closing is not the solution. What you can do is to pay off your balances but keep them accounts active.

5. Myth: Using too many credit cards could give you a bad score.

Fact: The moment you cancel your credit cards, you will be hurting your score more than you can expect.

Canceling your credit cards could certainly reduce your score because it signifies a shorter credit history for each. However, it could also hurt your score a lot if you are applying for a new credit card every week and then closing them one by one afterwards. The key to staying within the limits is to submit credit applications that you desire and keep them. Stick to the credit accounts that you truly desire and no harm will be done to your credit score.

4. Myth: Good payers are always given a fair rating.

Fact: Credit reports are erroneous 70% of the time.

Even if you have not done anything wrong and you have paid all your debts on time, your credit score could still go haywire. That’s because most of the time, erroneous details are entered into your credit report, which in turn produce a bad score. For all you know, you could be paying a significantly higher interest that you really need to.

3. Myth: Checking your credit report could hurt your credit score.

Fact: Checking could help boost your score by way of finding errors that are hurting it.

If you check your credit report, you will be able to keep track whether or not it is truthful. Faulty entries could hurt your credit score and correcting them could improve it. So there is no sense in stating that taking a peak on your credit report periodically could make your score go bad.

2. Myth: Your credit score will be the sole depending factor for all your loan applications.

Fact: The approval based on your credit score depends on what kind of loan you are applying for.

Lenders have different guidelines on the different loans they have on offer. If you want specific information on whether or not you are eligible for a specific kind of loan with a particular credit score, consult your bank or mortgage broker. It is important that you understand the lending guidelines that cover what you are applying for so you know exactly how you move.

1. Myth: Only one credit score is being used by lenders.

Fact: There are different credit scores that can be obtained about you; it depends on who is being asked.

Lenders use different scoring models that are available in the industry to help them measure your ability to pay your debts on time. The FICO or Fair Isaac Corporation scoring model is most popular but that does not mean it is the only thing out there.

April 17, 2013 6:31 am

Hi,

I am a content writer and I want to contribute a guest post for your blog on finance topic. I have contributed many articles for numerous websites. My article will be more than 400 words, informative, unique and it will only publish on your blog.

I will send my article as an attachment .txt file or in the word format.

Hope you would like my proposal and will give me an opportunity.

May I send my Article?

Regards,

Scott Mathew